The bullish oil market narrative is mired in a 1970s mentality, when oil shocks had large impacts on industrialised nations. This crisis will be different for two reasons. First, the impact will be heavily concentrated in East Asia. A prolonged disruption of shipments from the Mideast Gulf could depress East Asian GDPs by as much as three percentage points.

Second, developed nations will see only modest impacts because their economies are much less dependent on oil. Also, the leading OECD nation, the US, is now an oil and gas exporter. Thus, its overall economy will remain strong, lifting the economies of other OECD countries through trade despite the Trump tariffs. The impact on the US and other OECD nations is further reduced by the decline in the significance of the auto industry to their economies compared with 50 years ago. A decline in auto sales will not be much of an economic drag on them, as strong spending on AI and datacentres will bolster growth.

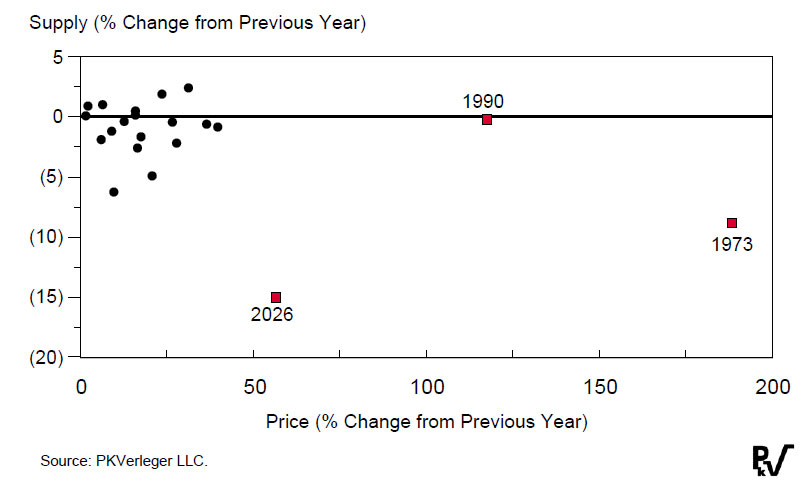

This crisis differs from the 1973 event and other major disruptions because the 2026 shortages are concentrated in the Asian market

The Strait of Hormuz oil shock has yet to crash demand as the rich world borrows from its stocks and pays up to secure supply. But traders are sounding the alarm that a harsh adjustment is coming. The longer the vital oil channel does not reopen, traders say, the more consumption is going to have to recalibrate lower to align with supply that has dropped by at least 10%. And for that to happen, people will have to buy less, either through prices they cannot afford, or government intervention to force consumption down.

A historical comparison suggests Brent might need to rise to $200/bl if this crisis follows the path set in 1973, given the supply reduction. The IEA puts this at 8m b/d, but its magnitude depends on how much oil is removed from stocks and on the duration of the Hormuz closure.

But this crisis differs from the 1973 event and other major disruptions because the 2026 shortages are concentrated in the Asian market, where the price elasticities of demand are higher and national economies are far more vulnerable to economic dislocations. For this reason, the price increases will be much smaller than in 1973, while the economic impacts on some nations could be much larger.

The impact of the war in Iran will likely resemble that of the 1997 Asian debt crisis, when economic activity plunged in Thailand, Indonesia and South Korea. Local GDPs fell by as much as 10% in a year, as did oil use despite oil prices falling by 50%, dropping to below $10/bl.

On this occasion, however, local GDPs will drop as oil prices rise. Higher prices will trim consumption somewhat, and those cuts will be compounded by declines in GDP. These developments will ease the need to reduce consumption in developed nations, particularly in EU countries, the US, Canada and Japan. This disparity may already be coming into view, with the first signs appearing in China.

The China shock

Chinese oil firms have all-but halted crude purchases in anticipation of being allowed to draw from stocks, and in response to strong bidding by competing refiners in Europe, according to information provider Argus Media. Chinese state-owned refiners have paused spot crude purchases—and even turned seller in some instances. Sinopec resold April-loading West African cargoes and at least 1m bl of May-loading Guyanese crude to Europe, Argus deal-tracking indicates. Chinese firms had earlier begun to repatriate equity production from regions such as Latin America including, unusually, Guyanese crude in response to energy security concerns triggered by the Hormuz crisis. They began reselling those cargoes as expectations mounted of being allowed to draw on commercial stocks, and because they are cutting refinery runs.

Chinese refiners had not entered into contracts to buy oil from Brazil for July delivery. Further, China cut nominations for May loading of Saudi term crude to around 580,000b/d, the lowest on record. Sinopec, the state oil company, and the jointly owned Chinese-Saudi refining company made the largest reductions.

On no other occasion over the past five decades have refiners in a nation reduced oil purchases or resold crude they were contracted to buy amid a disruption. In contrast, Korean buyers accepted delivery of Saudi Arabian crude in 1998 even as their domestic market collapsed, just to maintain a good relationship with the Saudis.

The development may be partially explained by the drop in Chinese demand during March and the expected further declines in the coming months. Argus puts the decrease at 1.5m b/d, almost double some estimates, and shows an 8% drop from the firm’s January–February average.

The decline may have accelerated in April. Chinese research firm Horizon Insight estimated China’s throughput at 13.4m b/d in the week to 17 April, down from 15.4m b/d in the week before the war started on 28 February. This would put the reduction at 2m b/d.

The higher gasoline prices in China may explain some of the fall-off in consumption. Retail prices there have risen by 28% since the disruption began, according to GlobalPetrolPrices.com. This might result in as much as a 10% decrease in gasoline use, according to a 2013 study of Chinese gasoline demand that estimated the price elasticity of demand at nearly –0.5. This elasticity is ten times larger than the short-term price elasticity of demand calculated by many economists, including this author, for gasoline in the US.

However, the price elasticity of demand in China may be even higher due to the widespread adoption of electric vehicles there. It seems possible that gasoline use might have declined by 500,000b/d from the 3.5m b/d estimated for February 2026.

The price elasticity for other petroleum products will be lower in China and other nations. Diesel fuel use, for example, is much less sensitive to price increases but very sensitive to changes in economic output. During the Asian debt crisis, diesel use fell by 200,000 b/d (4%) in Asia, accounting for roughly half of the reduction in the region’s oil product consumption.

The Asian burden

Asian refining throughput is set to tumble in April and May as crude imports hit a ten-year low and the Iran war forces refiners to process lighter grades, curbing diesel and jet fuel output by at least 1m b/d. Asia, which accounts for 37% of global refining output and ordinarily sources two-thirds of its crude from the Middle East, has been hardest-hit by the closure of the Strait of Hormuz, with run cuts at refiners in the region exacerbating tight fuel supply and keeping prices elevated.

The reduced volume of crude being processed already totals 2.7m b/d. Gasoline supplies will be particularly high and diesel output reduced as Asian refiners are forced to substitute lighter crudes for lost Middle Eastern supplies. Of the nearly 12m b/d of crude unable to reach Asia in March due to the effective closure of the Strait of Hormuz, nearly 8m b/d was of medium density and high sulphur content, or medium sours, which most Asian refineries are designed to process to maximise diesel output.

The crude oil grade change will cut the diesel yield from 60% per barrel to 40%f, according to some sources.

The uncertainty regarding the diesel supply loss is evidenced by the substantial differences in predicted impacts. Some analysts project a loss of 250,000–500,000b/d of diesel and jet fuel supply. Others put the losses at almost 2m b/d per day in April.

A statistical test revealed that a 5% reduction in diesel availability leads to a one-percent decline in GDP growth in East Asia. While it is naive to tie East Asia's economic growth solely to diesel supply, the results suggest that the supply cut could reduce growth there by one or two percentage points.

A comparison of changes in East Asia’s GDP and total oil consumption finds that a 1% GDP decline would lead to a reduction in oil use of 4m b/d. This suggests that, if East Asian growth falls by 2 percentage points in 2026 to, say, 1%, its oil use would decrease by 6–7m b/d.

The ‘Asia excluding Japan’ countries, then, look to bear 60–70% of the global oil consumption drop tied to the loss of Middle Eastern oil if the supply decline totals 10m b/d. The impact could also be half of that. Trading giant Gunvor Group estimates the loss could double next month to 5m b/d, or 5% of world supplies. The loss could double again if the strait remains closed through June.

This seems to imply that Asian consumers will use 3m b/d less if the Gunvor assumption is correct and possibly 5–6m b/d less if the disruption continues into the summer. The GDP shock, then, would be between one and two percentage points.

Modest suffering for the rest of the world

The general market view is that the entire world is confronting serious issues. Traders have suggested that the economic slowdown would be global. Some have compared the current shock to the 1973–74 events that thrust developed nations into recession. They may be correct on a barrel-per-day basis. However, the global economy has moved on, as the International Monetary Fund’s chief economist, Pierre-Olivier Gourinchas, explained at a press conference introducing the IMF’s projection of the Iran war’s economic impact.

After noting that the barrel loss was similar to that of 1973, Gourinchas added that: “There are, however, two important differences compared to that shock. The first one is that the global economy is much less oil‑dependent now than it was back then. There are many other sources of energy—renewables, nuclear, and other things—and also, the global economy has become much more efficient in terms of how much it needs oil to produce GDP. And so that’s a source of resilience, if you want.

Second, Gourinchas noted that central banks in 2026 were more attuned to inflation than in 1974. This focus on inflation expectations would hopefully prevent the impact of higher energy prices from spreading to all prices, boosting inflation and requiring monetary tightening that would exacerbate the depressing impacts of higher oil prices.

Gourinchas might also have noted a third change since 1974: the US’ shift from importing to exporting oil. The US economy suffered a recession in 1974 as higher oil prices and regulatory-induced fuel shortages affected most sectors of the economy. In December 1974, The New York Times reported on a study it commissioned to examine the impact of falling car sales on the US economy. The analysis showed that diminished sales resulted in a drop in employment of 630,000 workers, which accounted for 40% of the rise in unemployment from 4.3m in November 1973 to 6m in November 1974. The study also noted that the decline in auto sales was an important contributor to the economic downturn.

Professor James D. Hamilton offered a similar assessment in his Brookings paper on the 2008 oil price rise, asserting that the decline in auto sales began when high gasoline prices forced consumers to delay or forgo auto purchases. Ultimately, GM and Chrysler went bankrupt. While Hamilton’s view was not widely accepted, the change in auto sales was an important contributor to the Great Recession.

Today, the situation is different. Motor vehicle output accounts for only 2.4% of US GDP compared with more than 5% during the 1974 crisis. At the same time, investment in AI, datacentres, and the energy sector is surging. Thus, the impact of a severe energy disruption on the US economy will be negligible. The strength of the US economy, in turn, will lift economic growth in other nations to some extent through trade, especially if higher oil prices spur greater imports of manufactured goods. Hence, the impact of the oil disruption will be minimal for the US and probably the EU and Japan.

The price impact

As noted above, the current energy crisis is somewhat similar to the 1973–74 crisis when one focuses on the substantial oil price increases. In the earlier disruption, prices rose by more than 200% . However, through 24 April 2026, the crude price increase since the war began has only been 50% despite the loss of 13m b/d of supply. Brent would have to rise to $205/bl, up from the 24 April price of $111/bl, to match the 1974 increase. This is unlikely to occur for the following reasons.

First, as noted above, the current disruption’s impact will fall most heavily on East Asian nations. Second, consumption in these nations will fall quickly as their economies slow. Third, the price elasticity of demand in East Asian and OECD countries is almost certainly much higher than in the major oil-consuming nations in 1974. A doubling of the price elasticity relative to 1974 would cut the impact of the price increase in half, that is, back to around $110/bl. Fourth, lower-income nations in East Asia, Africa and South America will not have sufficient dollar liquidity to bid prices up to anything close to $205/bl. Instead, they will move rapidly to displace oil where possible and impose rationing where substitution is not possible.

Finally, the availability of various renewable energy sources and non-fossil-fuel-powered equipment—such as electric vehicles—will reduce oil use, thereby boosting the price elasticity of demand. Ultimately, $120/bl may be the price at which markets balance.

Dr. Philip Verleger received his PhD in Economics from MIT in 1971. He has studied energy and financial markets since. In 2023, Dr. Verleger was named 'Energy Writer of the Year' along with his editor Kim Pederson. Previous winners of the award include Daniel Yergin (2000) and Vaclav Smil (2019).